Spring 2023 Market Report: Stepping into spring

Despite the brake on house-price growth, the market, as well as economic outlook, is showing tentative green shoots as we head towards spring.

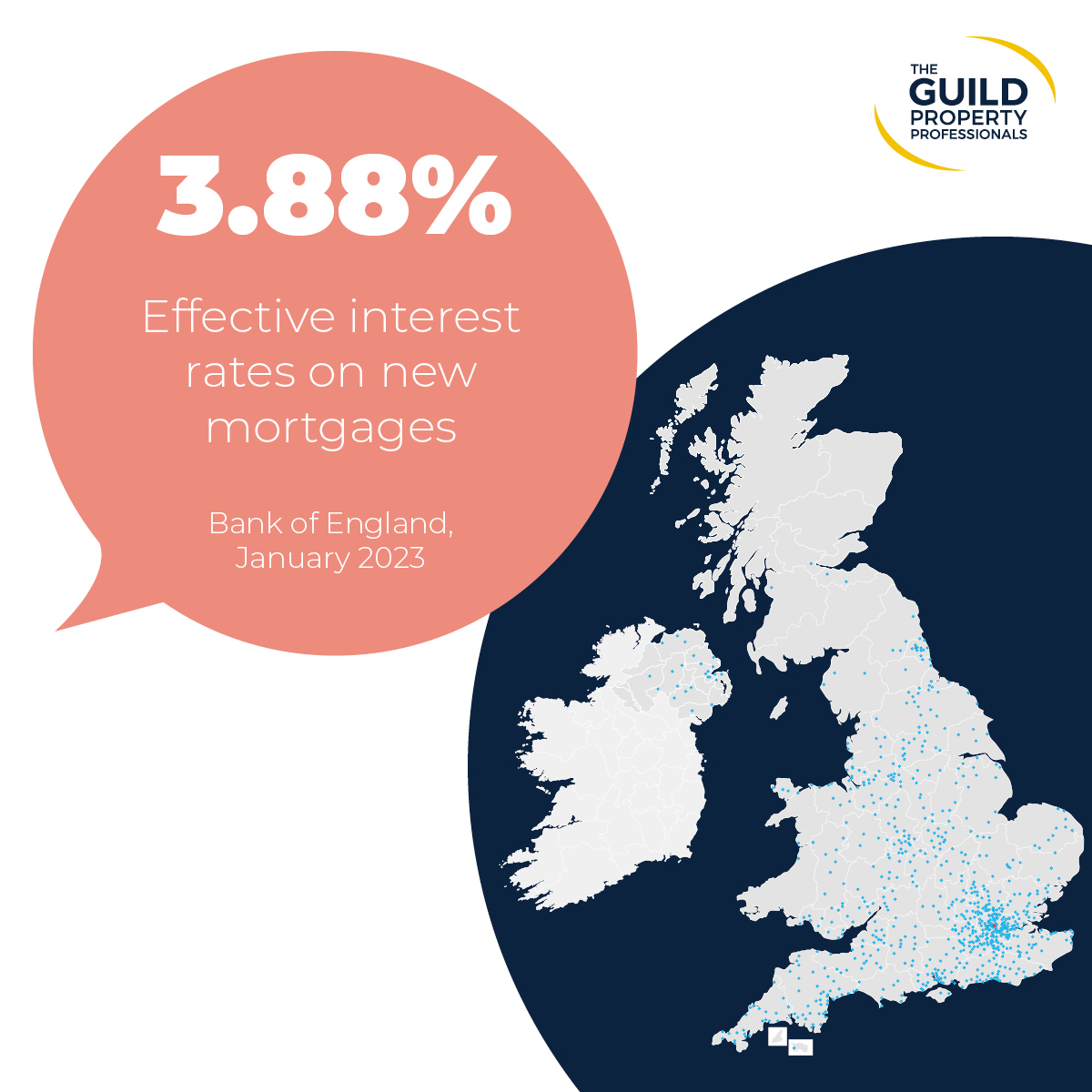

Mortgage matters

There has been a welcome fall in mortgage rates, with rates of below 4% for lower loan-to-value mortgages. Typical costs of a two-year deal and five-year fixed-rate mortgage have fallen back to where they were in October 2022, in spite of the Bank of England Bank Rate rising by 1.75% during this period. There has also been a rise in the number of mortgage products, with over 4,000 different products now available. The number of days a product is available before it is withdrawn has also increased, now at 28 days, up from just 15 days in January, the highest level since March 2022 (Zoopla).

Outlook

The housing market and economy are closely interlinked, and despite the rising cost of living, the rate of inflation has slowed and is expected to fall back over the course of the year. Employment levels remain strong, GDP forecasts are improving and any recession is

expected to be less severe than first predicted. Prices are softening but many sellers continue to be over-optimistic on price. With supply returning to more normal levels, up 60% compared to a year ago, there is more choice for prospective purchasers and Zoopla report the average discount to asking price is currently 4.5%.

Consumer confidence

The Bank of England announced that mortgage approvals in January had fallen to their lowest level since May 2020. However, there are more recent signs of improvement. Zoopla report that buyer demand is up 8% on the pre-pandemic years (2017–2019), while the latest survey of UK consumer confidence undertaken by GfK registered a +7 uptick in February. This represents the largest monthly improvement in nearly two years. Although still dented, confidence in the UK’s economic outlook and personal finances over the next 12 months registered a month-on-month rise of +11 and +9 points respectively.

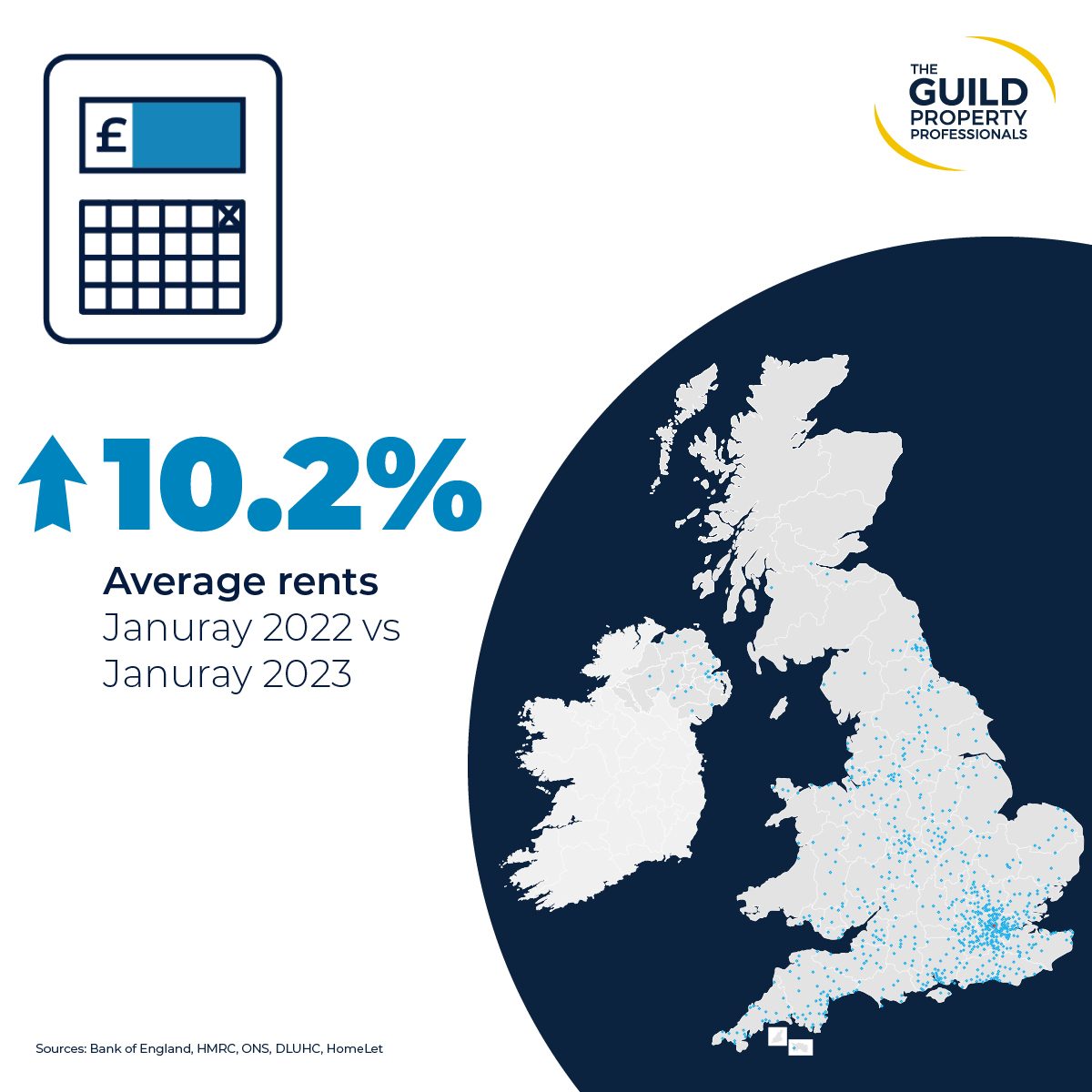

Signs of easing

Price growth in the rental sector is expected to continue in 2023. However, there are tentative indications that competition between renters, which has underpinned the record rental rises, is beginning to relent. Rightmove report that competition between renters for available properties has dropped by 6% compared with the same time last year, and a third compared with September’s peak. However, the imbalance between supply and demand remains high. The number of available homes to rent in the final quarter of 2022 was up 13%, while new-to-themarket properties are up 5% (Rightmove).

Regional Reports

Browse our Regional Market Reports:

● Market Report 2023 Spring East Midlands

● Market Report 2023 Spring Essex, Norfolk and Suffolk

● Market Report 2023 Spring Hertfordshire, Bedfordshire and Cambridgeshire

● Market Report 2023 Spring London

● Market Report 2023 Spring North East, and Yorkshire and The Humber

● Market Report 2023 Spring Northern Ireland

● Market Report 2023 Spring Scotland

● Market Report 2023 Spring Devon and Cornwall

● Market Report 2023 Spring Southern Home Counties

● Market Report 2023 Spring South East Home Counties

● Market Report 2023 Spring Southern

● Market Report 2023 Spring Thames Valley

● Market Report 2023 Spring West of England

● Market Report 2023 Spring West Midlands

● Market Report 2023 Spring North West

● Market Report 2023 Spring Wales

Contact us today

To see a full copy of The Guild’s winter market report and for further guidance on the home moving process, take a look at the regional property market updates or get in touch with your local Guild Member today.